Key Insights

- The profit from selling your home is called the capital gain.

- There are three conditions you must meet to be exempt from capital gains tax.

- You will most likely not have to pay capital gains tax if your profit is less than $250,000 (or $500,000 for married couples).

- You can estimate your capital gains by following a simple formula.

It may surprise you to know that many homeowners who sell their properties don’t end up having to pay capital gains taxes on the sale — even if they walk away from the closing table with a large sum of money.

While taxes can be complicated, and you should consult with your own tax advisor for your specific circumstances, there’s a general rule to help you determine if there will be tax implications when you sell your house, or if you will be able to keep the total amount earned. Read along for more insights as you navigate the taxes associated with selling a home.

Note: While this article covers the capital gains taxes that may be paid after a home sale, there are other taxes paid in connection with a sale, including a deed tax and certain property taxes. Consult your tax advisor for more information on these payments.

If I sell my house, do I pay capital gains tax?

After selling a home, the profit from the transaction is known as the capital gain. Sellers who wish to avoid paying capital gains taxes must:

- Have owned the property for at least two of the last five years.

- Have lived in the home for two of the last five years.

- Have not taken advantage of capital gain exclusion from another property sale in at least two years.

If all of these stipulations are met, home sellers can be excluded from capital gains up to $250,000 for solo owners (or for married couples who file separate tax returns) and $500,000 for married couples who file taxes jointly.

Many property sales don’t net more than these maximums. So, many home sellers in Minnesota and western Wisconsin don’t end up paying taxes on the gains they earned from selling.

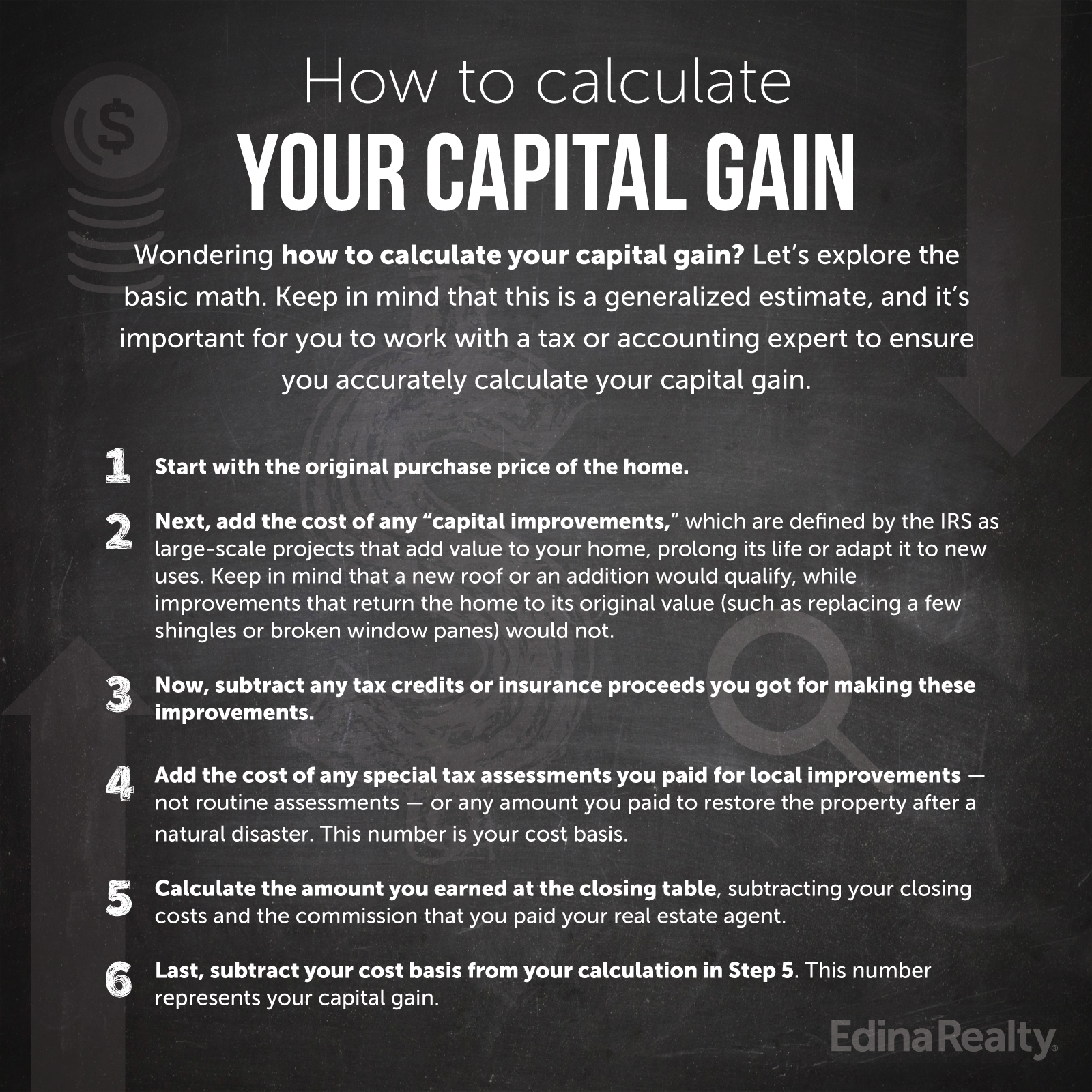

How to calculate your capital gain

Wondering how to calculate your capital gain? Let’s explore the basic math with some hypothetical numbers. Keep in mind that this is a generalized and hypothetical estimate for illustration only (your actual costs will vary). It’s important for you to work with a tax or accounting expert to ensure you accurately calculate your capital gain based on your actual costs.

1. Start with the original purchase price of the home.

$200,000

2. Then, add amounts you paid in conjunction with the purchase, such as title fees, transfer fees, inspection costs, real estate agent commission, etc.

+ $2,800

= $202,800

3. Next, add the cost of any “capital improvements,” which are defined by the IRS as large-scale projects that add value to your home, prolong its life or adapt it to new uses. Keep in mind that a new roof or an addition would qualify, while improvements that return the home to its original value (such as replacing a few shingles or broken window panes) would not.

+ $20,000 (New windows)

= $222,800

4. Now, subtract any tax credits or insurance proceeds you got for making these improvements.

- $3,500 (New window energy credit)

= $219,300

5. Add the cost of any special tax assessments you paid for local improvements — not routine assessments — or any amount you paid to restore the property after a natural disaster. This number is your adjusted cost basis.

+0 (No assessments needed!)

= $219,300 → This is your adjusted cost basis

6. Calculate the amount you earned at the closing table, subtracting your closing costs and any real estate agent commissions that you paid.

- $20,000 (Closing costs)

= $199,300

7. Last, subtract your adjusted cost basis from your calculation in Step 5 from the selling price. This number represents your capital gain.

$280,000 (Selling price) - $199,300 = $80,700

If at the end of this calculation, you’ve earned less than $250,000 (individual filing) or $500,000 (joint filing) and otherwise meet the exemption requirements mentioned previously, the final amount isn’t taxable — it’s just an asset that you’ve earned! You can use these funds to finance your retirement, put toward a new down payment or travel the world. See? The IRS isn’t always the enemy.

Keep in mind that when you are seeking to exclude your capital gains from tax obligations, you will need to have documentation of every number you submit to the IRS — from proof of the original purchase price and final sale price to the capital improvements and sale expenses you are claiming.

Be sure to keep receipts for any large repairs you take on yourself, as well as official documentation of the payments made to contractors, plumbers, roofers, HVAC companies, etc., who have helped you with capital improvements or restoration efforts made after natural disasters.

What if my capital gain is above the maximum allowed?

If your capital gain is above $250,000 (or $500,000 for a couple filing jointly), then you will have to pay capital gains taxes on the sale of your home for the amount above the exclusion. The amount you owe will be determined based on your capital gain, as well as what tax bracket you fall into.

Remember, calculating capital gains taxes can be a complicated process — especially if you are selling a home for the first time or aren’t sure what updates count toward home improvements. Be sure to consult a tax advisor to help ensure you calculate and pay the correct amount.

Are there any deductions I can take advantage of if I sell my home at a loss?

Unfortunately, losses incurred from the ownership of a private residence aren’t tax deductible. So while you won’t have to pay taxes on the sale of your home, you also won’t earn anything back in the form of a tax deduction or credit.

Is there a way to avoid paying capital gains taxes when selling an investment or vacation property?

The capital gains exclusion only applies if you meet the three criteria mentioned above, which likely would not apply to an investment or vacation property. Some homeowners who own rental properties or vacation homes do avoid paying capital gains taxes when selling their property by moving into their home permanently for two years before they sell it and making sure to spread their home sales out by two years. Also, if you are selling an investment or business property and are planning to purchase a similar property, you may qualify to defer the capital gain under what is called a 1031 exchange.

Other than that, you may have to pay a capital gains tax on the sale of a secondary property. Remember, tax fraud is a serious crime — so you should never claim that you lived permanently in a home if you didn’t.

Key points and next steps

Do these hypothetical numbers have you calculating your own home sale or considering what you’d do with the profits? Don’t go it alone! Reach out today for your custom home value estimate.

©2026 Prosperity Home Mortgage LLC®. (877) 275-1762. 3060 Williams Drive, Suite 600, Fairfax, VA 22031. All first mortgage products are provided by Prosperity Home Mortgage, LLC®. Not all mortgage products may be available in all areas. Not all borrowers will qualify. NMLS ID #75164 (For licensing information go to: NMLS Consumer Access at

©2026 Prosperity Home Mortgage LLC®. (877) 275-1762. 3060 Williams Drive, Suite 600, Fairfax, VA 22031. All first mortgage products are provided by Prosperity Home Mortgage, LLC®. Not all mortgage products may be available in all areas. Not all borrowers will qualify. NMLS ID #75164 (For licensing information go to: NMLS Consumer Access at